Renewables set for a variable-speed takeoff as historic investment, competitiveness, and demand propel their development, while also exacerbating grid, supply chain, and workforce challenges.

In a bifurcated renewable landscape, the solar market brightened in 2023, while wind faced sweeping challenges. The latter bore the brunt of project inputs, labor and capital cost pressures, interconnection and permitting delays, and transmission limitations. Meanwhile, supply chain constraints started easing as historic clean energy and climate laws took effect.

In the United States, utility-scale solar capacity additions outpaced additions from other generation sources between January and August 2023—reaching almost 9 gigawatts (GW), up 36% for the same period in 2022—while small-scale solar generation grew by 20%.1 Only 2.8 GW of wind capacity came online during the same period, down 57% from last year, resulting in renewables accounting for just over half of capacity added versus two-thirds last year.2 However, renewable energy’s share of US electricity generation remained level at 22%.3 By the end of 2023, the US Energy Information Administration expects utility-scale solar installations to more than double compared to 2022, to a record-breaking 24 GW, and wind capacity to rise by 8 GW.4

The tandem push of federal investments flowing into clean energy and pull of decarbonization demand from public and private entities have never been stronger. Moving into 2024, these forces could enable renewables to overcome hurdles caused by the seismic shifts needed to meet the country’s climate targets. The uplift and obstacles shaping the year ahead have set the stage for a variable-speed takeoff across renewable technologies, industries, and markets.

TABLE OF CONTENTS

- Regulatory boosts and brakes

- Reshoring clean energy

- Reskilling the workforce

- Renewables as a resilience strategy

- Renewable technology, redefined

- The future

Federal investment push

Deployment highs. The Energy Information Administration expects renewable deployment to grow by 17% to 42 GW in 2024 and account for almost a quarter of electricity generation.5 The estimate falls below the low end of the National Renewable Energy Laboratory’s assessment that Inflation Reduction Act (IRA) and Infrastructure Investment and Jobs Act (IIJA) provisions could boost annual wind and solar deployment rates to 44 GW to 93 GW between 2023 and 2030, with cumulative deployment of new utility-scale solar, wind, and storage reaching up to 850 GW by 2030.6

Cost lows. A temporary rise in renewable costs could belie their long-term declining trend and relative competitiveness. High financing, balance of plant, labor, and land costs outweighed commodity and freight price falls in 2023, pushing up the levelized costs of energy (LCOEs) for wind and utility-scale solar, especially projects with trackers that account for 80% of installed solar capacity.7 Inflation and interest rates disproportionately impacted offshore wind, which saw a 50% rise in its LCOE from 2021 to 2023.8 While this equation may prevent LCOEs from resuming historical downward trends in 2024, the IRA investment tax credits and production tax credits have made utility-scale solar and onshore wind, including projects paired with storage, competitive with marginal costs of existing conventional generation.9 Projects claiming the maximum available credits could capture the world’s lowest solar and wind LCOEs.10 Renewables collecting production tax credits will likely increase the prevalence of negative prices in wholesale electricity markets.11

Decarbonization demand pull

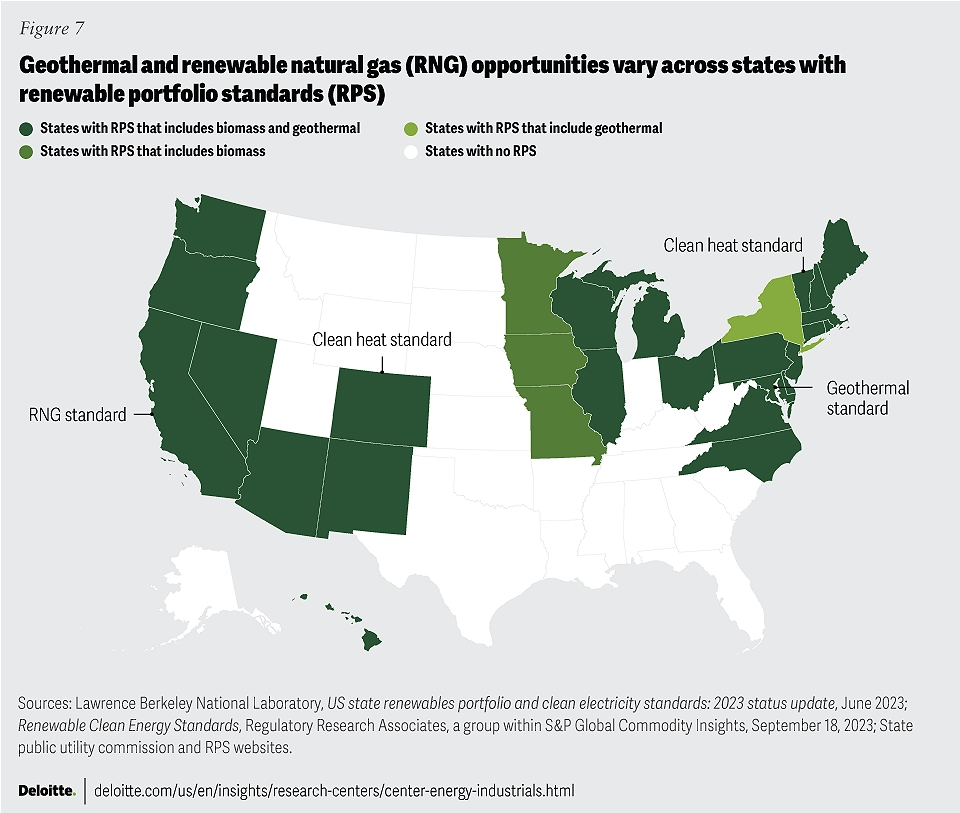

Most states and utilities. Twenty-nine jurisdictions, representing around half of US electricity retail sales, have mandatory renewable portfolio standards (figure 7); 24 jurisdictions, including two new states in 2023, have zero greenhouse gas (GHG) emissions or 100% renewable energy goals spanning 2030 through 2050.12 Renewable portfolio standards and clean energy standard policies are expected to require 300 terawatt hours (TWh) of additional clean electricity by 2030.13 Complementary to state goals are the 56 individual and 28 parent utilities with carbon reduction targets that serve 83% of US customer accounts.14 Twenty-five utilities have further committed to either an 80% carbon reduction or an 80% share of clean generation by 2030.15 More states, localities, and public utilities are expected to invest in renewables in 2024, as the IRA’s direct pay and transferability mechanisms help enable their market participation.16

Major corporations. In the first 10 months of 2023, 30 companies joined RE100, a global corporate initiative to procure electricity entirely from renewables, growing the membership to 421.17 Around a quarter of the members are headquartered in the United States, and a bulk of their upcoming commitments have a 2025 target date. Some are also driving decarbonization throughout their supply chains. Following a record-breaking year, corporate renewable procurement saw the number of transacting customers increase by 31% between the first half of 2022 and that of 2023.18 Big technology companies accounted for most of the procured capacity19—a trend likely to grow in 2024 as the companies meet and help others meet 24/7 and carbon-matching targets with the help of generative artificial intelligence.20 The training and use of generative AI could increase their data center demand for clean electricity five- to sevenfold.21 A growing number of corporations are also expected to support renewables by participating in the nascent tax-credit transfer market in 2024. Coming full circle, corporations are participating in multinational efforts to push governments to address climate change and accelerate the energy transition. Ahead of COP28, 131 companies with close to US$1 trillion in annual revenue drove a campaign urging governments to phase out fossil fuels by 2035.22

The impact of unprecedented investment in renewable infrastructure will likely become more apparent in 2024. Regulatory boosts to renewable energy and transmission buildout could help address grid constraints. And boosts to manufacturing could lay the foundations of a domestic clean energy industry with stronger supply chains supporting solar, wind, storage, and green hydrogen deployment. A skilled workforce should be prepared to build, operate, and maintain all these new generation and manufacturing facilities planned over the next few years. As renewables become a larger part of power generation and the portfolio of technologies grows, perceptions could start catching up with the reality that renewables can enhance grid resilience. Deloitte’s 2024 renewables industry outlook discusses how these trends could impact the industry in the coming year:

- Regulatory boosts and brakes: Historic investment could erode obstacles

- Reshoring clean energy: Supply chains shorten and strengthen

- Reskilling the workforce: Unlocking the talent bottleneck is key to decarbonization

- Renewables as a resilience strategy: Amid widespread misperceptions, renewables can save the day

- Renewable technology, redefined: Underground renewables could resurge

{kind=link}

1. Regulatory boosts and brakes: Historic investment could erode obstacles

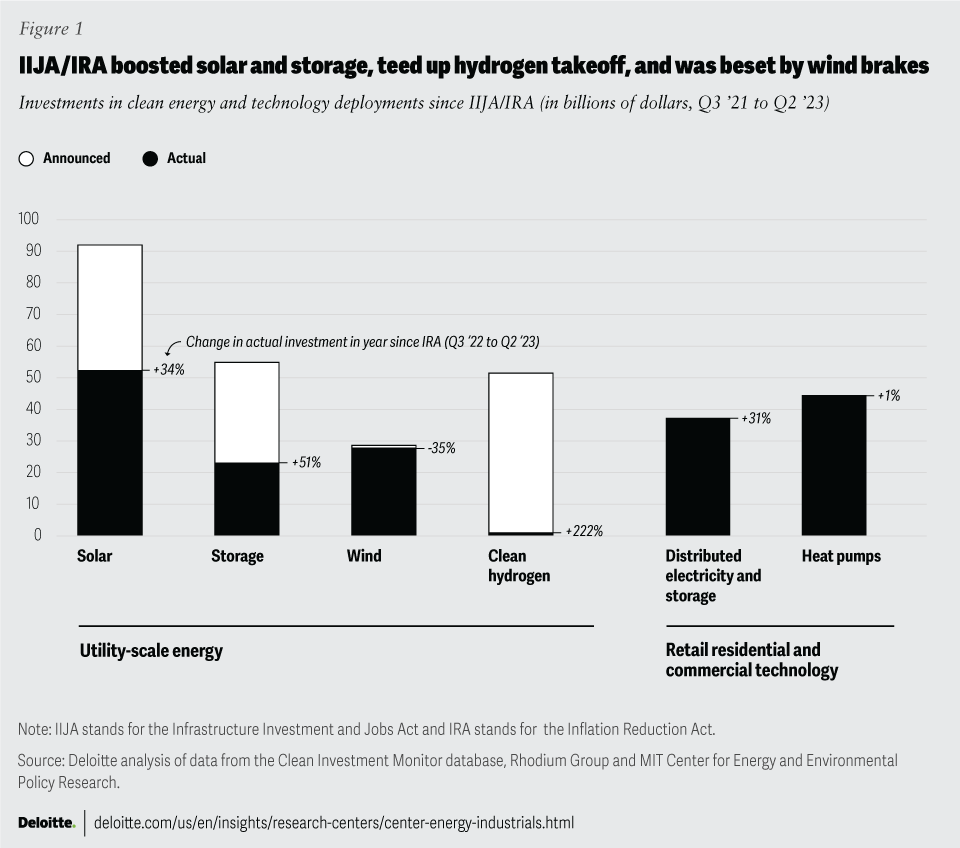

The IIJA and the IRA have boosted renewables through historic investment in new or expanded programs, grants, and tax credits to accelerate the deployment of established and emerging renewable technologies. Over the past two years, they helped catalyze US$227 billion of announced public and private investments in utility-scale solar, storage, wind, and hydrogen.23 To date, US$100 billion of these investments have materialized, in addition to US$82 billion in distributed renewables and heat pumps (figure 1). States also offered a record US$24 billion in tax breaks in 2022 to attract projects.24 The bulk of investment flowed to states with ambitious decarbonization targets and mandates, led by California, as well as states with greater renewable resources and lower permitting and siting costs, led by Texas and Florida.25 An outsize share of clean energy investment also flowed to energy, disadvantaged, and low-income communities identified in the IRA for additional incentives.26

{kind=link}

Solar and storage soar

The IIJA and the IRA have had some of the biggest impacts on solar and storage. Utility-scale solar captured the largest share of both announced investment of US$92 billion and actual investment of US$52 billion across 38 states. The month after the IRA passed, a record 72 GW of standalone solar was added to the interconnection queue, more than the preceding 11 monthly additions combined.27 Amid a venture capital (VC) industry slowdown, VC funding for solar and storage increased in the first three quarters of 2023, and the IRA boost blunted higher interest rates as public market and debt financing for solar also grew.28 Solar recorded 34% growth in actual investment over the past year, storage jumped 51%, and distributed renewables, storage, and fuel cells increased 31%.29

IRA tax credits have allowed solar and storage developers to creatively configure projects around siting and grid constraints through standalone or hybrid deployment. In 2024, tax credit adders are expected to shape solar and storage market offerings.30 US Treasury’s release of guidance on energy and low-income community adders in the last quarter of 2023 could be particularly relevant to community solar developers.31 The guidance may also drive more third-party owned solar and storage projects, which can qualify for these adders unlike customer-owned systems.32 Finally, the impact of US$7 billion in Greenhouse Gas Reduction Fund grants should be seen through the Solar For All program and the US$3 billion loan from the Department of Energy’s (DOE’s) Loans Program Office (LPO), which is the government’s largest-ever single commitment to solar.33 Both programs focus on distributed solar and storage deployment in low-income and disadvantaged communities.

Hydrogen teed up for takeoff

The IIJA and the IRA have teed up the takeoff of a new green hydrogen economy. Clean hydrogen has the largest gap between announced and actual investments—more than US$50 billion and less than US$1 billion, respectively.34 The gap reflects in part uncertainty over pending Treasury guidance on tax credits that are expected to make green hydrogen competitive. At stake is whether hourly matching, additionality, and deliverability will be required to qualify for the full US$3/kg credit.35 Favorable final guidance could open the floodgates on actual investments in 2024 and jumpstart the nascent hourly Renewable Energy Credit (REC) market. Treasury alignment with the European Union’s approach to gradually phase in the three requirements could also enable the US industry to serve the 10 million metric tons (MMT) clean hydrogen import market that the EU envisions by 2030.36 Exports could help resolve demand uncertainty reflected in the DOE’s reallocation of US$1 billion in hydrogen hub funds to stimulate demand.37 In 2024, the industry should watch for developments in the seven selected hydrogen hubs as they move into their design and planning phase, as well as the launch of the country’s first end-to-end green hydrogen system.38

Energy efficiency inches up

Investment following the IRA fell short of meeting ambitious targets for energy efficiency, as reflected in heat pump deployments. While heat pumps attracted close to US$45 billion, investment has only grown 1% over the past year.39 Final DOE guidance on state administration of direct customer rebate programs could unleash growth in 2024. An initiative of the US Climate Alliance of 25 states to install 20 million heat pumps by 2030 could further bolster deployments,40 as could utility-funded energy efficiency programs.41

Wind brakes

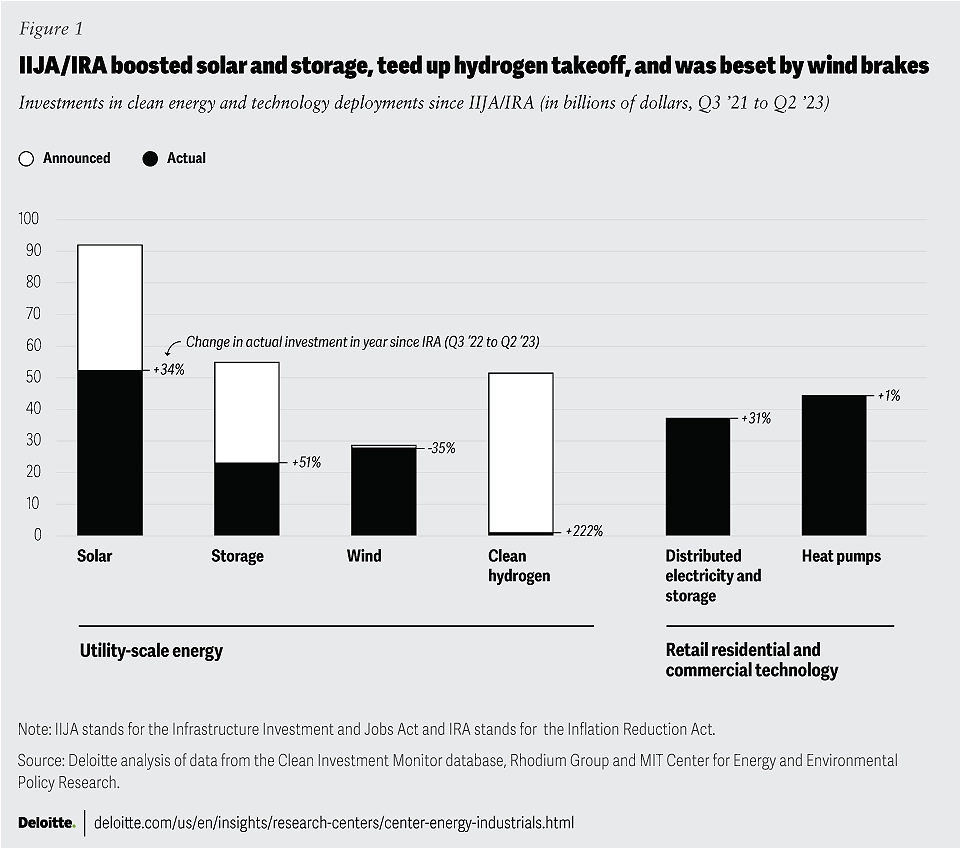

Wind investment dropped 35% over the past year as projects bore the brunt of headwinds from higher costs and permitting challenges, which respondents of a Deloitte survey identified as the most significant constraints on renewables (figure 2).42 Record curtailments felled wind in most independent system operators (ISOs).43 And of the 55 GW in delayed clean power projects, wind projects are facing the longest delays, stretching out to 16 months.44 An increase in local and state restrictions and contestations of renewable projects over the past year also impacted wind more than other sources (see the sidebar titled “Generative AI’s impact on renewable deployment bottlenecks”).45

Generative AI’s impact on renewable deployment bottlenecks

While generative AI is being used to generate climate disinformation, fueling some of the opposition to renewables, it is also powering new tools for developers to assess community sentiment toward renewables and automate permitting and siting.46 For the latter, generative AI can help select the best locations for renewable energy installations, considering wind patterns, solar exposure, and environmental impact. It can also suggest the best solar panel layout to maximize generation and design the most efficient blades with peak aerodynamics for wind. In 2024, more developers are expected to use generative AI tools to inform and accelerate renewable project decisions, processes, configurations, and community engagement.

Offshore wind faces high capital requirements, long project development and permitting timelines, and locked-in power sales contracts.47 Developers executing agreements signed during low inflation now face higher financing costs and 40% jump in equipment and construction costs over the past year, while state policymakers may not be willing to provide additional support that could increase consumer costs.48 Four contract renegotiations and three cancellations have imperiled half the of the offshore wind pipeline.49 Federal and state action to expedite permitting, ease financing, and adjust incentives may be needed to keep projects in the pipeline and on track for meeting targets.

In 2024, the tide is expected to start turning as the industry gets more steel in the water and adapts to the new seascape. Developments to watch include the start of operations at Vineyard Wind in Massachusetts;50 the construction of the country’s largest offshore wind project in Virginia;51 the Oregon, Central Atlantic, and second Gulf of Mexico lease sales;52 and the pursuit of coordinated procurement in three northeastern states.53 Flexible structures and market participants are expected to reshape agreements. Following Treasury guidance, more developers may seek to improve project economics by siting onshore grid connections in the energy communities that line US coasts and qualify for an adder.54 There may also be greater uptake of the adder from the growing pipeline of onshore wind-repowering projects since most are located in energy communities.55

Tackling transmission

Transmission is a factor in most constraints on renewable deployment. Regarding the top cost constraint survey respondents identified (figure 2), capturing the full customer benefit of low-cost renewables hinges on transmission. Insufficient capacity drove up congestion costs by 72% in 2022 over the previous year to US$20.8 billion.56 Interregional and regional transmission would need to more than double and quintuple, respectively, to meet high clean energy growth projections by 2035.57

IIJA and IRA programs and grants could start tackling transmission issues in 2024. These include the DOE’s announced plans to accelerate high-voltage transmission line permitting,58 US$3.9 billion in grants from the Grid Resilience and Innovation Partnerships Program,59 and US$1.3 billion in grants for three interregional grid projects.60 At the beginning of the year, we’ll be watching for the DOE’s release of additional Transmission Facilitation Program funding and US Federal Energy Regulatory Commission interconnection rule compliance plans, as well as complementary ISO initiatives to reduce interconnection queues.61 We expect to see more corporations participate in Federal Energy Regulatory Commission regulatory filings as transmission constraints jeopardize their renewable targets.62 At the same time, IRA and IIJA boosts to renewable development could significantly exacerbate pressure on transmission bottlenecks in 2024.

{kind=link}

2. Reshoring clean energy: Supply chains shorten and strengthen

A domestic clean energy manufacturing revival is underway as producers reshore to better capitalize on IRA tax credits and meet demand from renewable developers chasing domestic content adders. Since the IRA passed, companies have announced US$91 billion of investments in over 200 manufacturing projects, including US$9.6 billion in 38 solar projects, US$14.4 billion in 27 storage projects, US$1.4 billion in 14 wind projects, and US$54 million in six hydrogen projects, closely tracking investment levels in their respective renewable energy sources.63 These projects’ shortened supply chains could increase transparency and resilience while decreasing emissions and exposure to geopolitical vicissitudes.

Solar and storage set to surge downstream and start extending upstream

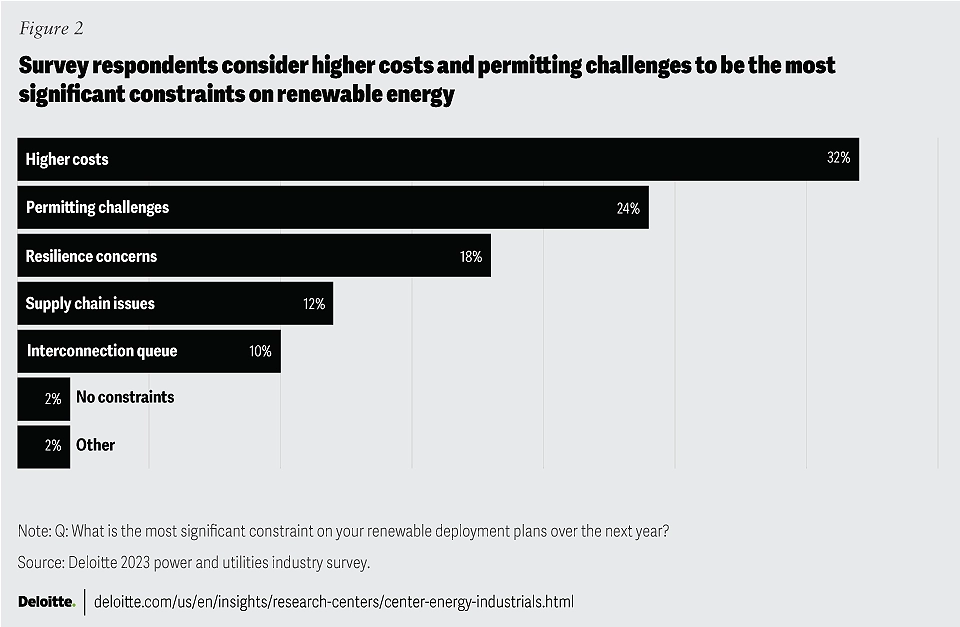

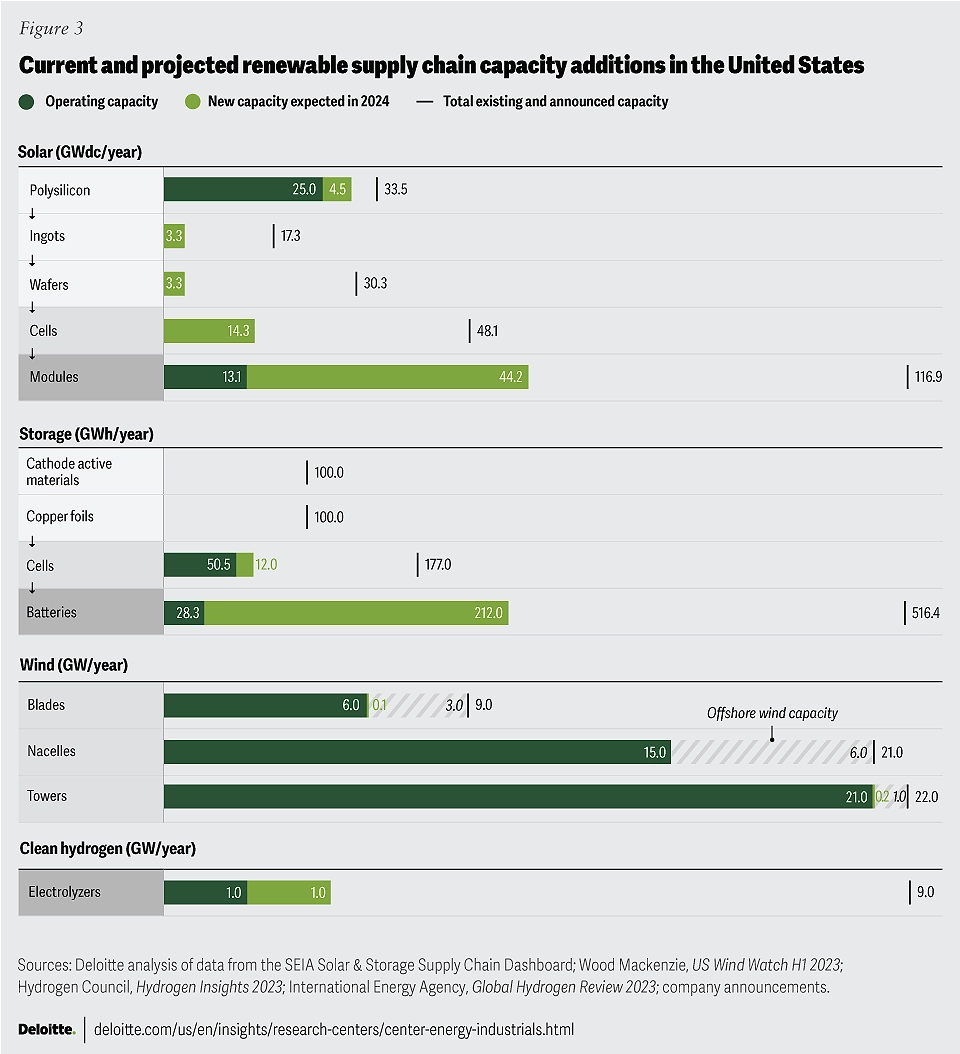

Announced projects could more than triple this year’s solar photovoltaic module capacity in 2024, grow it by an order of magnitude by 2026, and meet US demand before 2030 (figure 3)64—a striking reversal from US import dependence for 85% of supply in 2022.65 While China currently produces 83% of the cells and polysilicon and 97% of the wafers that go into modules,66 new domestic polysilicon capacity and the United States’ first cell, wafer, and ingot manufacturing plants are slated to come online in 2024.67 This reshoring is premised on balancing domestic panels’ 40% price premium68 and the 40% tax incentive69 for manufacturers that use 40% domestic components.70 The latter part of this equation may be at risk because 40 GW of module capacity planned by 2025 may not qualify for a domestic content adder due to lack of sufficient cell capacity.71 Meanwhile, solar imports more than doubled in the first eight months of 2023 amid global overcapacity that drove prices to record lows, placing half the pipeline at risk of delays or cancellation.72 In 2024, the enforcement of trade rules and the Uyghur Forced Labor Prevention Act73 and the expiration of waivers on duties covering solar cell and module imports from Southeast Asia in June74 could address overcapacity concerns. And more far-reaching final Treasury guidance on the domestic content adder could encourage upstream investment in wafers, ingots, and polysilicon.

{kind=link}

Storage is on a similar trajectory as solar. Announced projects could drive almost eightfold growth in battery manufacturing capacity in 2024. Planned cell production could grow the US share of global capacity from 4% in 2022 to 15% by the end of the decade in a segment where China currently holds a 79% share.75 Yet, lithium-ion battery imports also reached a record high in 202376 and the US continues to be fully dependent on imports for some upstream supply chain components.77 Companies have announced projects to manufacture copper foils and cathode active materials, 100 GWh for each, but none are expected to come online in 2024.78 Expanded Uyghur Forced Labor Prevention Act enforcement on batteries could provide further impetus to domestic supply chain development in 2024.

Wind homes in on offshore gap

The wind supply chain is more domestically rooted and evenly distributed across components than solar and storage, but the little capacity change planned for 2024 may be raising concerns offshore. China leads the global market for wind too: With turbines selling at prices 70% lower than their Western counterparts, Chinese manufacturer exports jumped to 70% of wind turbine orders announced in the first half of 2023.79 The greater role of developer relationships, specifications, and incentives in offshore wind has relatively insulated its supply chain from import pressure. On the other hand, infrastructure development and capacity additions have lagged demand from offshore wind developers seeking access to domestic content adders that could improve project economics. Meeting the Biden administration’s offshore wind target could require a US$22.4 billion investment in 34 additional manufacturing facilities, 10 dedicated vessels, and 10 ports.80 Whether projects proceed in 2024 hinges on the offshore wind pipeline’s solidity. The development of 18 planned component manufacturing facilities81 and the collaboration between nine East Coast states and federal agencies on offshore wind supply chain buildout are anticipated.82

Hydrogen electrolyzers take root

Electrolytic hydrogen is embryonic at a time when industrial policy is ascendant and the global production landscape is still in flux, providing a major opportunity to reshore renewables. The high-efficiency electrolyzers that dominate the US pipeline are more economic, despite higher upfront costs, but they are exposed to competition from low-cost manufacturing regions.83 China is already expected to account for over half of global capacity in 2023.84 In the United States, companies have announced 9 GW of electrolyzer manufacturing capacity, under a quarter of which is expected to come online in 2024.85 Most projects remain at early stages as the market awaits Treasury guidance on green hydrogen that could trigger a burst of electrolyzer demand.86 The Department of Energy (DOE) estimates electrolyzer capacity would need to grow at a 20% compound annual growth rate to meet demand through 2050.87 In 2024, we will be watching the relative competitiveness of manufacturers focused on scale versus modular approaches, and their ability to keep pace with demand. Gaps could prompt domestic content requirements for electrolyzers.

Critical mineral crimp tightens

The IRA has driven up energy transition demand for the critical minerals that underpin renewable supply chains. By 2035, this demand is expected to rise 15% and 13% higher than pre-IRA numbers for lithium and cobalt, respectively, which are needed for storage; 14% for nickel, which is in storage, wind, and hydrogen supply chains; and 12% for the copper needed across all energy transition technologies.88 Meanwhile, domestic and free trade agreement country supply that could qualify for IRA incentives is limited. China refines around half of global copper production, two-thirds of lithium, three-quarters of copper, and four-fifths of nickel.89 And Indonesian nickel, which accounts for half of global mining capacity, is mostly Chinese invested.90 Underinvestment in mining amid currently low prices, combined with long lead times for new projects that can stretch over a decade, could yield yawning supply gaps. Shortages ranging from 10% to 40% across these minerals are expected by 2030.91 In 2024, the impact of China’s graphite export controls on critical mineral projects should be observed. The beginning of massive shifts in the lithium market from both the supply and demand sides may also become apparent. The discovery of the world’s largest known lithium deposit in Nevada at the end of 2023 is a potential game-changer.92 And the development of lithium alternatives, such as sodium storage batteries, could accelerate as manufacturers use generative AI to develop new molecules for testing.93

Trends to watch as renewable energy companies reshore in 2024 include the following:

- Companies are pursuing strategic reshoring joint ventures to secure a stake in the emerging domestic supply chain. For example, one of the largest renewable developers holds majority ownership and agreement to offtake 40% of output from a new solar panel plant that it is jointly developing with a solar manufacturer.94 And a major solar manufacturer became the largest shareholder of a US polysilicon manufacturer, striking a 10-year take-or-pay agreement that helped restart the plant’s production.95 Critical mineral mining projects are also seeing direct investments from customers.96

- Supply chain digitalization is helping companies increase transparency, efficiency, and awareness of competitor demand. It can enable monitoring of environmental, social, and governance practices and compliance with labor and US and free trade agreement content requirements under the IRA and the Uyghur Forced Labor Prevention Act.

- Clean energy manufacturers are developing end-of-life management and recycling of solar panels, wind blades, batteries, and electrolyzers to reduce waste and recover critical minerals.97 Battery-metal recycling startups raised record funding in 2022.98 Since the IRA passed, six companies have announced investments in battery and wind blade recycling.99 Two have received Loans Program Office conditional loan commitments. These projects could help address critical mineral shortages.

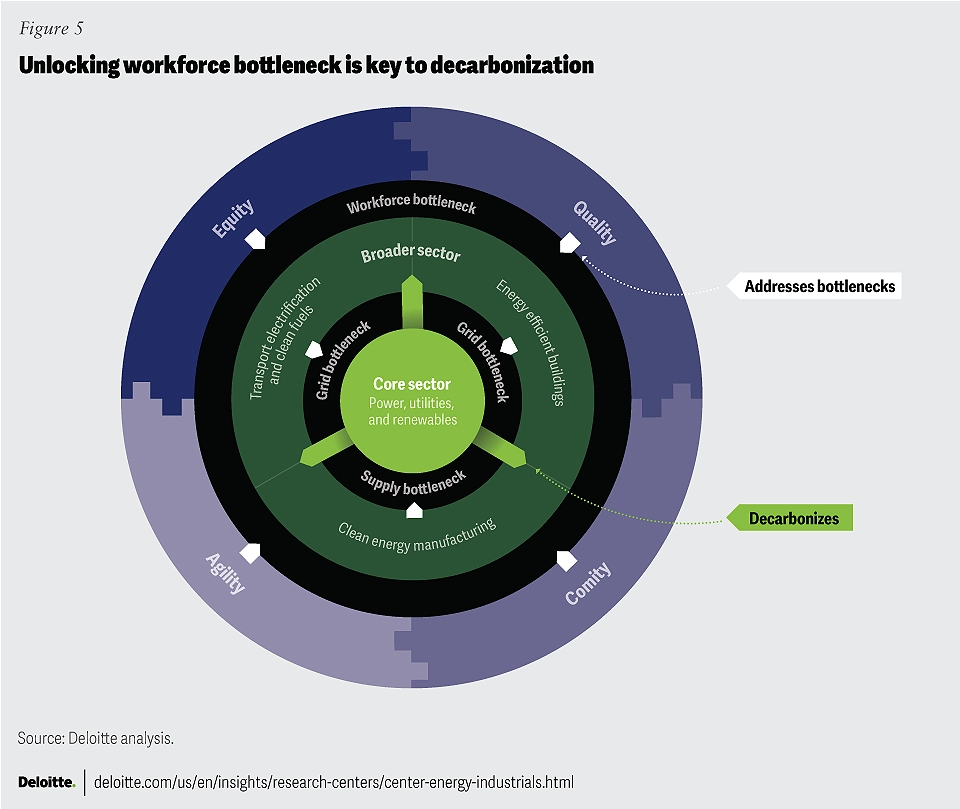

3. Reskilling the workforce: Unlocking the talent bottleneck is key to decarbonization

Sustaining a record buildout of renewables and domestic supply chain will require growing and (re)training a workforce with the right skills in the right places. Over the past two years, clean energy jobs have grown 10%, at a faster pace than overall US employment.100 There are currently 3.3 million clean energy jobs, the majority of which are in energy efficiency (68%), followed by renewable generation (16%), clean vehicles (11%), and storage and grid (5%).101 Looking ahead, wind turbine service technicians and solar photovoltaic installers bookend the projected 15 fastest-growing occupations from 2022 through 2032, when IRA provisions are scheduled to sunset, with 45% and 22% growth, respectively.102

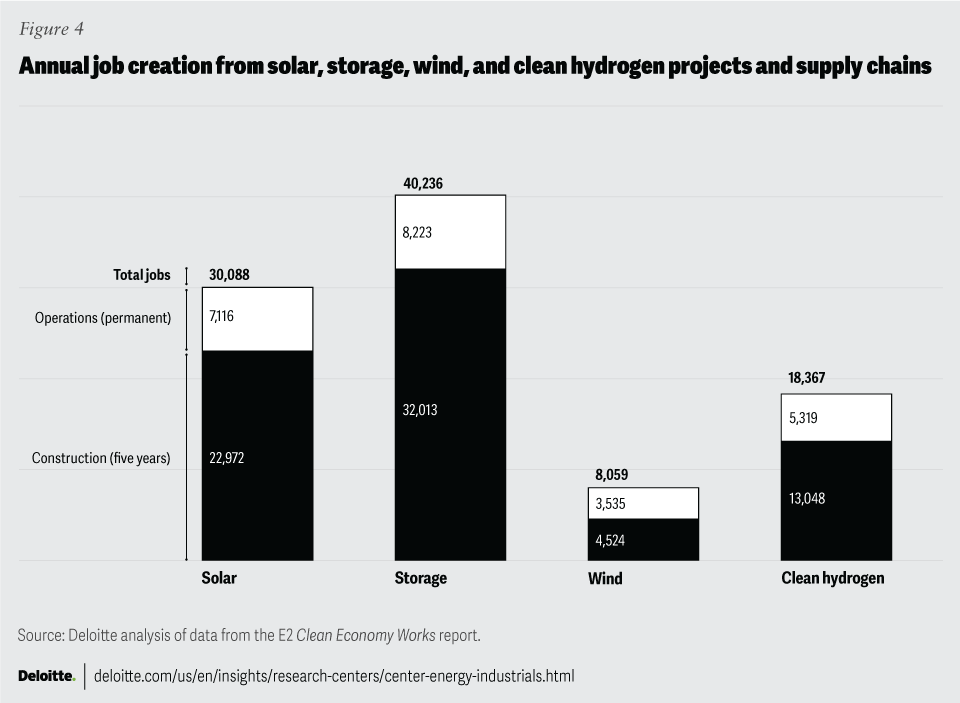

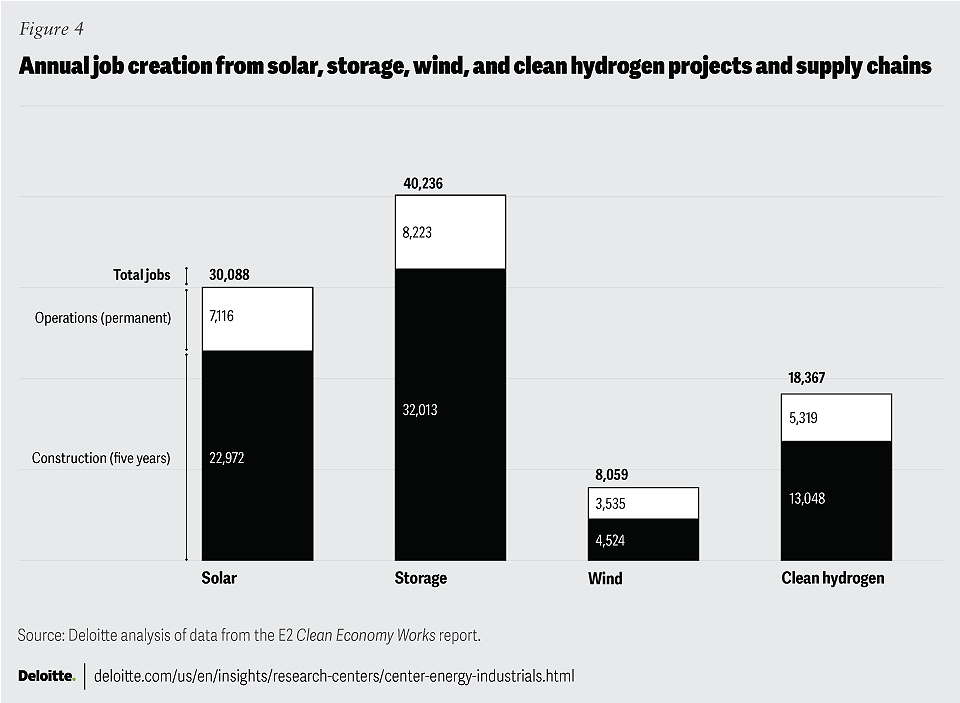

The IRA, the IIJA, and the Creating Helpful Incentives to Produce Semiconductors Act are expected to drive massive job creation over their lifetime: 19 million job-years, or around 3 million jobs per year.103 Compared to jobs in the overall workforce, a higher share—more than two-thirds—of direct jobs are available to workers without a bachelor’s degree. The direct jobs created offer higher-median wages on average, but benefits and unionization rates are lower, and women and other minority groups are underrepresented, according to current data.104 Announced manufacturing and generation projects across solar, storage, wind, and clean hydrogen plants and their supply chains anticipate the creation of 72,557 annual construction jobs over five years and 24,193 annual operations and maintenance jobs over the lifetime of the plants (figure 4). However, the current half-a-million workforce shortage in the construction sector could constrain the buildout.105 And while US green job postings grew 20% in 2022, green talent only grew 8.4%, revealing a growing skills gap.106

{kind=link}

Workforce challenges may be greatest in new industries such as clean hydrogen. The seven hydrogen hubs, expected to create 324,280 direct jobs across 16 states, include multiyear workforce plans to address these challenges.107 More immediately though, the 3.6 GW of currently funded electrolyzer capacity is slated to start coming online in 2024.108 The new facilities are expected to create around 12,000 infrastructure development jobs over the next two years, as well as 1,600 permanent operational jobs.109 Deloitte analysis identified skill gaps across core roles and found that there is already a shortage of workers with the required skills, including electrical engineering, manufacturing processes, computer science, tooling, mechanical engineering, automation, and machining.110 And the training pipeline for the relevant workforce of welders, machinists, and engineers across higher education institutions, including two- and four-year colleges, technical, and trade schools, shows potential talent supply challenges in three of the host states.

Generative AI is also reshaping renewable workforce needs. The solar and wind electric power generation industry includes five of the top 10 most AI-intensive occupations—that is, occupations with the largest share of job postings demanding AI skills.111 The most significant of these occupations in the industry are engineering professionals. Talent acquisition for these roles is already challenging, given the competition with other sectors.112 In the administrative segment, generative AI facilitates the submission of daily work orders, supply part requests, asset maintenance, and bidding.113 The core construction and maintenance workforce segments have the lowest penetration potential, 6% and 4%, respectively.114 Here, AI is enabling full automation of the sector’s most arduous work, such as offshore wind turbine inspections, which AI-powered drones could perform on spinning turbines at a lower cost.115 At a broader electric and gas utility level, while most occupations have generative AI exposure, five occupations, including core electrical powerline installers and repairers, have none.116

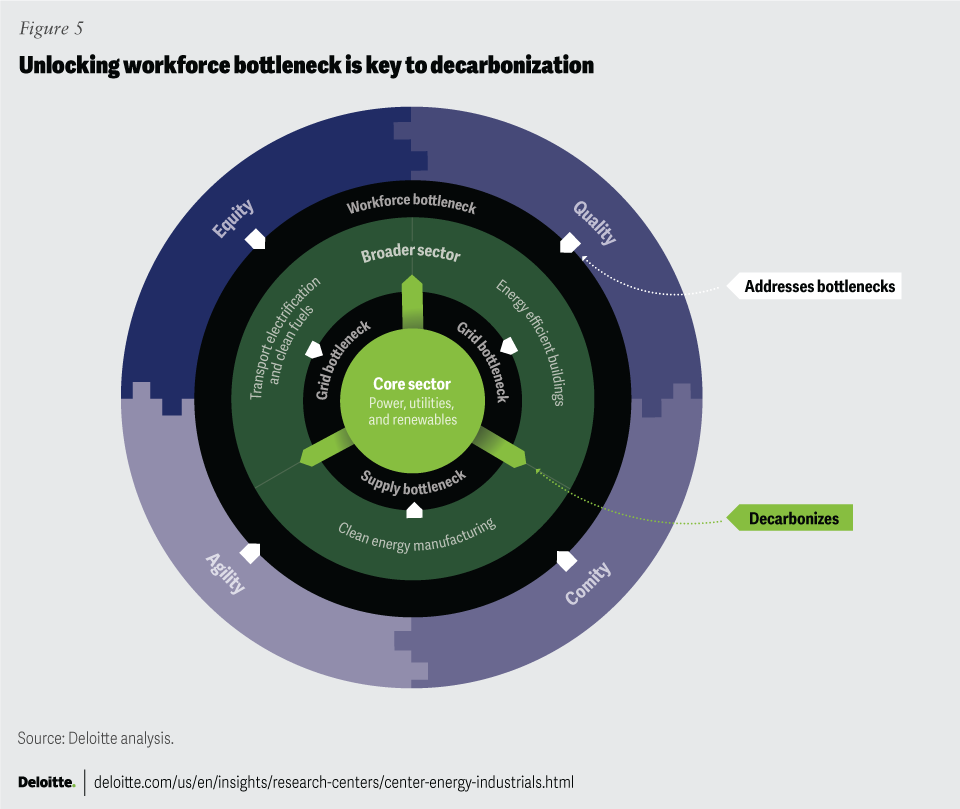

It is crucial that the core power sector, including power, utilities, and renewable developers, align their decarbonization and workforce planning to ensure the sector is able to continue decarbonizing itself and other sectors such as transportation, buildings, and manufacturing (figure 5). These sectors are helping address some of the bottlenecks constraining the core power sector. For example, transportation electrification, clean fuels, and energy-efficient buildings can help address grid bottlenecks, while domestic clean energy manufacturing should help address supply chain challenges. However, the workforce bottleneck encompasses both the core and broader sectors.

{kind=link}

More developers are expected to implement strategies with the following four following elements to help unlock the workforce bottleneck in 2024:

- Equity: Upskill the existing workforce in energy communities and help create new, diverse talent pipelines from local, untapped labor pools alongside workplace accommodations to address spatial, identity, and family structure inequities.

- Quality: Create purposeful, high-wage, credentialed jobs with portable skills and clear upwardly mobile career paths.

- Agility: Continuously assess skills gaps and training timelines (in weeks, months, and years), and proactively align with decarbonization strategy and technology timelines, the pace of domestic supply chain development, and the pace of digitalization, including the use of AI in the sector.

- Comity: Collaborate with ecosystem partners, including educational institutions, trade schools, high school career academies, and technical training groups; local, state, and federal governments; unions; industry associations; and philanthropic organizations to help develop registered apprenticeships, courses, and small business training support.

In 2024, the US Treasury’s final guidance on prevailing wage and apprenticeship requirements should take hold and help facilitate a pipeline of renewable energy apprentices that could alleviate shortages. Also anticipated is greater renewable developer and utility uptake of funding from the 54 IIJA and IRA programs that can be deployed for green workforce development.117

4. Renewables as a resilience strategy: Amid widespread misperceptions, renewables can save the day

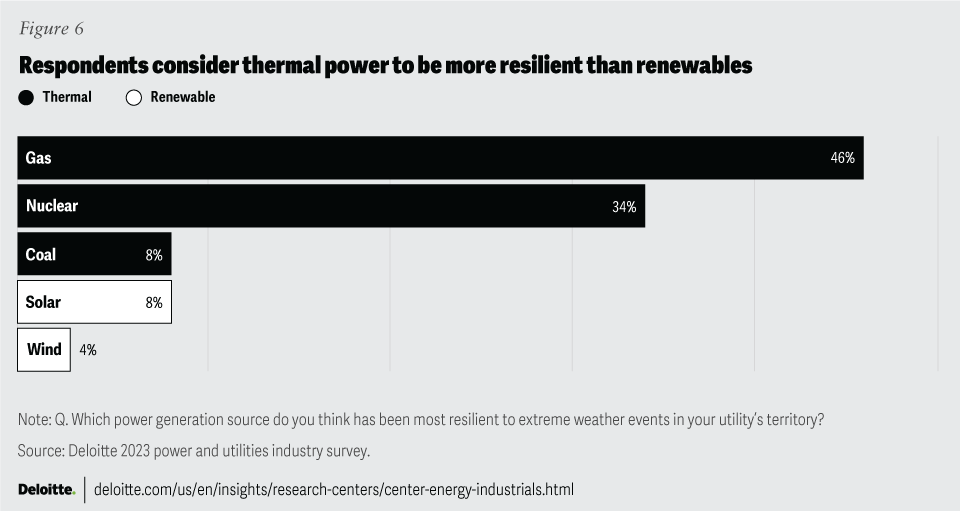

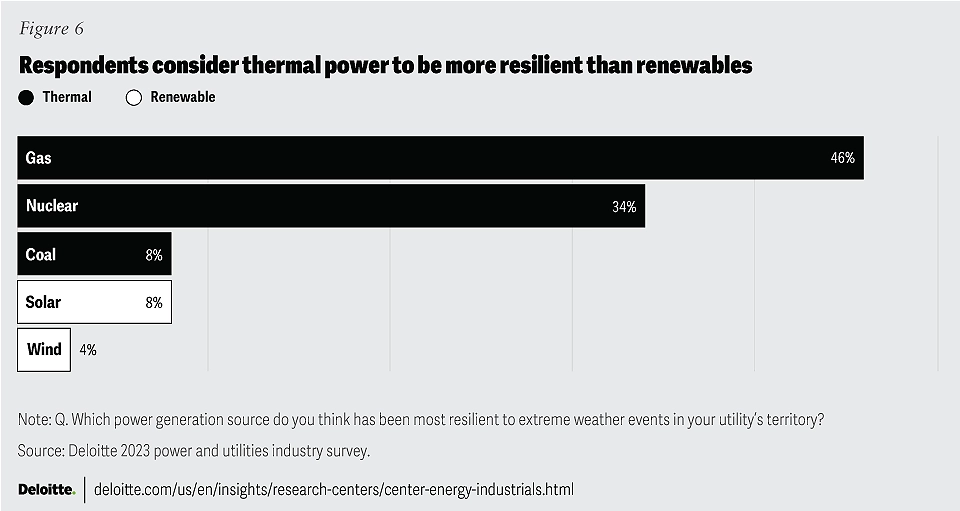

As the frequency and intensity of extreme weather events, outages, and potential electricity supply shortages rise, renewables have often outshined conventional power sources, generating electricity when the latter could not. Renewables are increasingly becoming a resilience strategy, especially when coupled with storage. This reality does not match with perception, however. More respondents of the Deloitte 2023 power and utilities industry survey were concerned about the resilience of renewables than supply chain challenges and the interconnection queue. Most survey respondents believe that gas, followed by nuclear power, is the most resilient to extreme weather events in their territory, while renewables ranked the lowest (figure 6).

{kind=link}

But, in contrast to the surveyed respondents’ perception, experience with a record number of extreme weather events and outages over the past year shows that gas poses greater reliability challenges than renewables. For instance, during Winter Storm Elliott, unplanned generation outages reached a record 90.5 GW across the Eastern Interconnection, mainly driven by natural gas infrastructure reliability issues.118 The impact on the Pennsylvania-New Jersey-Maryland Interconnection (PJM) was especially striking given the grid’s historical reliability, familiarity with cold weather, and location atop shale gas basins that directly supply many power plants. A fifth of gas plants, including new ones, failed to ramp up to half capacity during the grid’s two emergency calls due to a range of malfunctions across the system, from mechanical problems to frozen transmitters, valves and wells, pipe pressure issues, compressor stations failures, and supply scheduling gaps.119 Gas accounts for 46% of PJM capacity, but drove 70% of forced outages.120 Shifting seasons and states, in the summer, thermal plant outages unexpectedly went above the 11,000 MW red line, which, according to the Electric Reliability Council of Texas (ERCOT), could put its grid at risk.121

Nuclear also faces increasing reliability concerns as warmer and lower water levels caused by climate change impact operations. Over the past summer—a season when nuclear is most needed to meet power demand—a hot weather alert factored into a shutdown of the nuclear Vogtle plant reactor in July.122 Another nuclear plant shut down later in the summer due to coolant leakage, contributing to a total of 31 unplanned nuclear outages from January through October 2023 and a 25% rise in total nuclear capacity outages in the summer of 2023 versus that of 2022.123

Meanwhile, renewables paired with storage are taking on the role of gas peakers that can quickly respond to demand spikes and avoid blackouts. During Winter Storm Elliott, strong wind generation helped the Midcontinent Independent System Operator meet demand and continue exports despite 49 GW of forced outages.124 When Texas experienced 10 demand records this summer, batteries discharging in the evening played a key role in avoiding blackouts, while solar and wind generation covered more than a third of demand load in ERCOT during the day and helped prevent power price spikes.125 As a result, ERCOT included storage for the first time as a resource able to meet high net load in its fall Seasonal Assessment of Resource Adequacy for fall 2023.126 Similarly, renewables contributed to a fifth of generation during a heatwave that drove record loads in the Southwest Power Pool.127

On the distributed renewable front, when the California Independent System Operator called for electricity conservation on August 17, an aggregation of 2,500 residential storage systems were activated for the first time to deliver 16.5 MW of solar power to the grid.128 Some utilities are subsidizing residential battery installations to create such AI-orchestrated aggregations to draw on during peak demand.129 In the aftermath of winter storms and flooding, the Vermont Public Utility Commission lifted caps on programs supporting residential storage the utility can tap during emergencies.130 Meanwhile, generative AI is enabling greater solar photovoltaic module power forecasting and proactive mitigation of extreme weather and cyberattacks.131 In its latest forecast, the North American Reliability Corporation not only warned about an elevated risk of blackouts across the country this winter,132 but also showed that some states rapidly transitioning to renewables are among those at lowest risk of outages.133 The year 2024 may be when perception catches up with reality.

5. Renewable technology, redefined: Underground renewables could resurge

Technologies expected to become more apparent over the next year are transforming renewable capabilities, synergies, and deployment potential. Renewable deployment over the past decade has primarily told a success story for onshore wind, solar, and storage growth amid dramatically falling cost curves. On the flip side, the intermittency and the geographical land use and industrial end-use limitations of renewables are often cited as reasons these resources cannot replace gas as a direct and back-up fuel that can be deployed anywhere and tapped anytime. Yet, renewables that can do just that while supporting grid resilience have made strides this year in moving technological innovation toward commercialization. Two of these renewables are longstanding but often overlooked underground resources: geothermal and renewable natural gas (RNG).

Enhanced geothermal systems (EGS) have expanded the potential to capture the heat of the earth. While the United States is the global leader in geothermal electricity production, geothermal only accounts for 0.4% of US utility-scale generation and is concentrated in Western states, with natural hot water reservoirs in permeable rock at low depths.134 EGS could push this share past 6% by 2035, the target date for a 90% cost reduction in EGS, to US$45/MWh under the DOE’s Enhanced Geothermal Earthshot initiative.135 EGS uses technology from the oil and gas industry to help create artificial reservoirs and access the omnipresent heat available below the earth’s surface. Cost reductions are achieved from advanced sensing and drilling, which accounts for half the cost of geothermal projects.136 Developer use of generative AI to assess seismic data and guide drilling has further driven down costs.137 EGS can also bring more value by using reservoirs for long-duration storage and direct air capture. This year saw breakthrough announcements from the DOE-funded Frontier Observatory for Research in Geothermal Energy and geothermal energy startups on demonstrating commercial viability and breaking ground on the world’s largest EGS plant. While geothermal accounts for less than 3% of power purchase agreements (PPAs), the megawatt (MW) volume of geothermal PPAs quintupled from 2021, when the world’s first corporate geothermal PPA was signed, to 2022; next-gen geothermal accounted for more than half of the MW volume in 2023.138 The EGS project pipeline and PPA market are likely to continue strengthening in 2024 to meet demand from the growing number of corporations with 24/7 decarbonization targets.

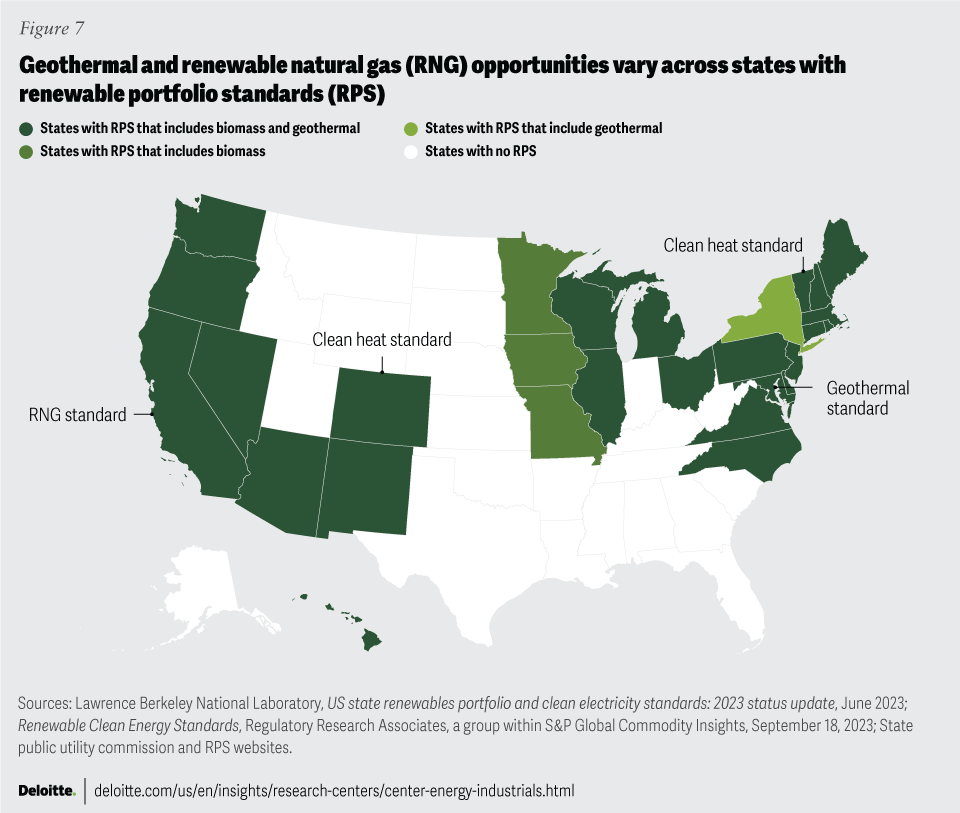

RNG project development has accelerated recently as well. RNG only accounts for 0.5% of the gas market and mostly serves the transportation sector but could grow tenfold by 2050 as usage expands to power and heat.139 Demand has overtaken supply as developers seek to begin construction on RNG facilities before 2025 to qualify for the IRA Section 48–qualified biogas property investment tax credit. The number of operational plants jumped from 230 in 2021 to 300 through the end of July 2023, while the pipeline of plants planned or under construction grew from 172 to 481 for the same period.140 Landfill and livestock operations are driving most of RNG capacity growth anticipated to come online in 2024.141 These two sources of feedstock account for more than half of US methane emissions, which RNG production can prevent from being vented.142 Food waste and wastewater treatment projects are also growing. New feedstock streams that could start expanding in 2024 may include forest waste from vegetation management related to wildfire prevention. The use of RNG as a feedstock to produce biohydrogen and sustainable aviation fuels could also take off depending on Treasury guidance on the hydrogen tax credit and carbon accounting. Two major US hydrogen projects are currently using RNG to produce hydrogen.143 Also important to consider is US Environmental Protection Agency rulemaking that could grant renewable credits for RNG used in plants generating power to charge electric vehicles. States with supportive policies could further increase RNG demand (figure 7).

In 2024, renewable developers may consider expanding into renewable resources resurging with new technologies. Geothermal and RNG can help developers diversify their renewable portfolios and capitalize on new synergies between intermittent and baseload renewables, and between electrons and molecules.

{kind=link}

What to expect in 2024

In 2024, the renewable energy industry could expect to see the historic climate legislation take greater effect as tax credit guidance is finalized, more Loans Program Office loans are issued, and more programs release IRA grant funding, only 10% of which has been disbursed thus far.144 The massive public and private investment and channeling of capital toward the clean energy transition could propel solar and storage deployments to continue soaring, onshore wind to recover, and residential technologies to pick up speed. Offshore wind and green hydrogen industries could establish a foothold, while underdeveloped renewables could play a greater role in clean energy portfolios. Meanwhile, a clean energy–driven manufacturing renaissance could provide opportunities to develop more resilient renewable supply chains across the country. The surge in renewable projects and domestic manufacturing also calls for a bigger and smarter grid, a skilled workforce to build and operate the plants, and a smooth process to develop both. Challenges in these areas should be addressed in 2024 to help keep the country and corporations on track to achieve their climate goals.

Signposts to watch include the US Treasury’s guidance on hydrogen and domestic content adders, the impact of IRA and IIJA funds on workforce development, and Federal Energy Regulatory Commission and DOE actions on grid reform and buildout. This El Niño year may bring more extreme weather events that could call on renewable resources to support the grid. Finally, a quickly expanding range of use cases may grow generative AI’s foothold in renewable operations, workforce planning, and distributed aggregations supporting resilience.

Originally published by Deloitte.